Debt-to-Income Ratio (DTI) Explained: How It Impacts Your Mortgage Approval

Debt-to-Income Ratio (DTI) Explained: How It Impacts Your Mortgage Approval

Your Credit Is Strong. Your Savings Are Solid. So Why Did the Bank Say No?

You did everything right. Your credit score is healthy. You’ve saved for a down payment. Your income is steady.

Then the lender declines your application.

In many cases, the issue isn’t your credit. It isn’t your savings. It’s your debt-to-income ratio, also known as DTI.

DTI is one of the most common reasons mortgage applications are denied. You can earn a good salary and still get turned down if too much of your monthly income is already committed to other debts.

Before you apply for a mortgage, it’s critical to understand this number, how lenders use it, and how to improve it if needed.

A Quick Checklist Before You Apply

Before speaking with a lender, make sure you:

- Know your current DTI

- Avoid opening new credit accounts

- Hold off on financing large purchases

- Keep your employment stable

- Consider paying down high-interest debt first

- Save additional cash if possible

These steps alone can prevent months of frustration.

What Debt-to-Income Ratio Really Means

Your debt-to-income ratio compares how much you owe each month to how much you earn each month before taxes.

Lenders use DTI to answer a simple question: Can you realistically afford another monthly payment?

If most of your gross income is already going toward car loans, student loans, and credit cards, adding a mortgage increases the risk that you could struggle to keep up. That risk is what lenders are trying to manage.

The Two Types of DTI Lenders Look At

Front-end DTI measures only your housing costs. This includes your projected mortgage payment, property taxes, homeowners’ insurance, and any HOA dues.

Back-end DTI includes everything: housing costs plus car loans, student loans, minimum credit card payments, personal loans, child support, and other recurring debts.

When lenders talk about DTI limits, they usually refer to the back-end DTI ratio. That gives them the full picture.

A Simple Example

Let’s say you earn $6,000 per month before taxes.

If your total monthly debt payments, including your future mortgage, equal $2,000, your DTI is:

$2,000 divided by $6,000 = 33 percent.

That means one-third of your gross income goes toward debt payments. Most lenders consider 33 percent manageable.

How to Calculate Your Own DTI

Step 1: Add Up Monthly Debts

Include:

- Car loans

- Student loans

- Credit card minimum payments

- Personal loans

- Home equity loans

- Child support or alimony

Do not include:

- Groceries

- Utilities

- Insurance premiums

- Gas

- Streaming subscriptions

Only include required monthly payments that show on your credit or legal obligations.

Step 2: Determine Your Gross Monthly Income

Use your income before taxes. Divide your annual salary by 12.

If you receive bonuses, commissions, or self-employment income, lenders usually require a two-year history before counting it fully.

Stable, consistent income matters more than temporary spikes.

Step 3: Divide and Convert to a Percentage

Divide total monthly debt by gross monthly income. Multiply by 100.

That number is your DTI.

What Lenders Include and Exclude

Included in DTI:

- Mortgage payments

- Car loans

- Student loans, even if deferred

- Credit card minimum payments

- Personal loans

- Home equity lines

- Court-ordered payments

Not included:

- Rent you will no longer pay

- Utilities

- Groceries

- Car insurance

- Health insurance

- Phone bills

- Subscriptions

Even if you pay off your credit card every month, lenders still count the minimum payment.

What DTI Do Lenders Want?

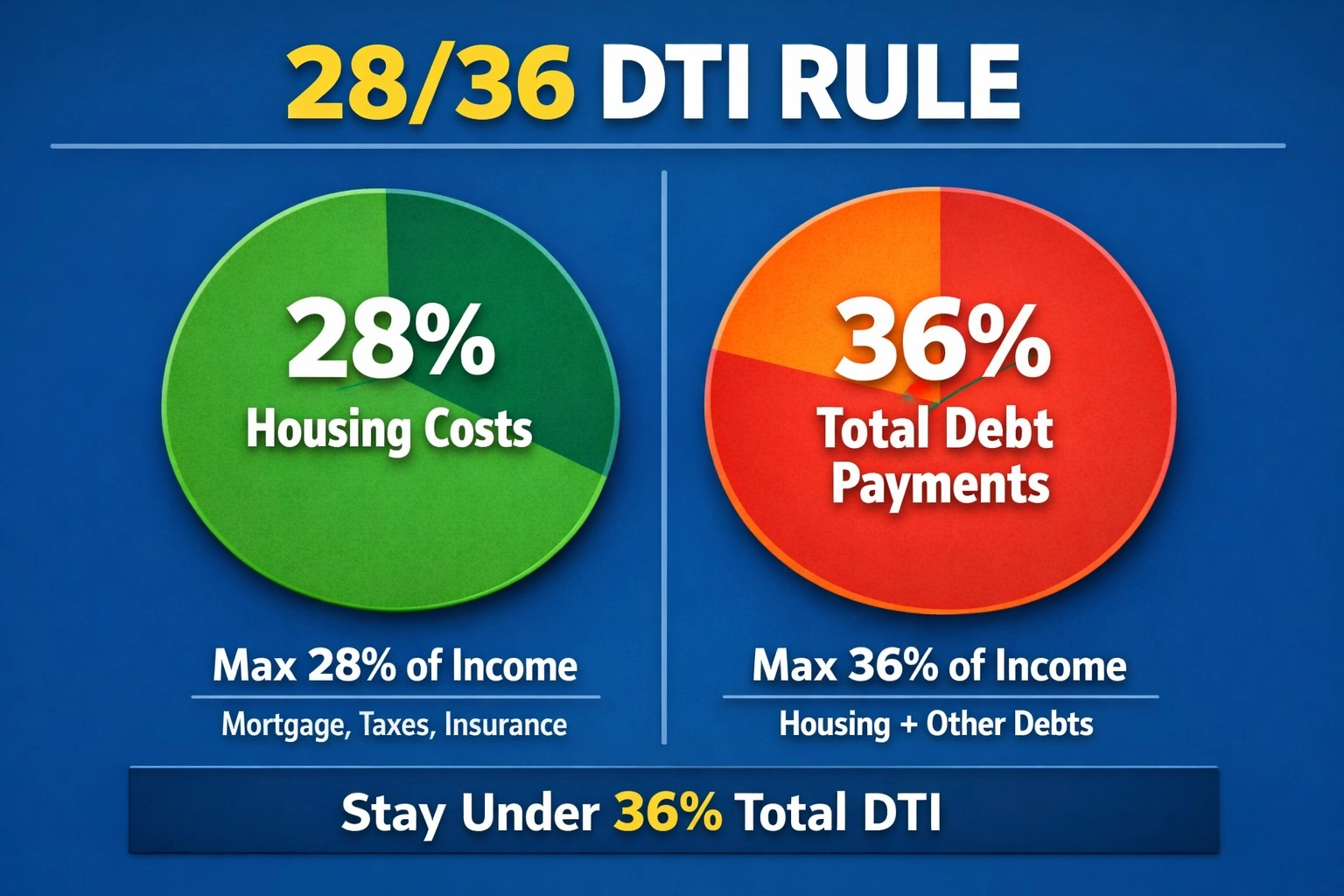

Many financial advisors reference the 28/36 guideline.

The 28 percent rule suggests your housing costs should not exceed 28 percent of your gross income.

The 36 percent rule suggests that total debt payments should remain below 36 percent of gross income.

In reality, lenders often approve higher ratios depending on the loan type.

Conventional loans may allow up to 45-50% in some cases.

FHA loans may allow up to 43 percent, sometimes higher with strong credit.

VA loans provide flexibility, though 41 percent is often referenced.

USDA loans generally look for ratios around 41 percent.

Just because you qualify at a higher percentage does not mean it is comfortable. Qualification and affordability are not the same thing.

What Happens If Your DTI Is Too High?

A high DTI does not automatically mean denial, but it creates obstacles.

You may:

- Receive a smaller loan approval than expected

- Be offered a higher interest rate

- Be required to put more money down

- Be asked for additional documentation

Even small interest rate increases can cost thousands over the life of a loan.

How to Lower Your DTI Before Applying

Pay Down High-Interest Debt First

Credit cards typically carry the highest interest rates. Reducing those balances can improve both your DTI and your credit score.

Some people use the avalanche method, targeting the highest interest rate first. Others use the snowball method, paying off smaller balances first to build momentum. The important thing is progress.

Increase Income Where Possible

While not always easy, increasing income helps.

Consistent overtime, documented side income, or a raise can strengthen your profile. Keep in mind that lenders often require a two-year history for variable income.

Avoid New Debt

This is critical.

- Do not finance a car before closing.

- Do not open new credit cards.

- Do not make large purchases on store credit.

Even a $300 monthly payment can push your DTI above approval thresholds.

Other Factors Still Matter

DTI is important, but it is not the only factor.

- Credit score influences approval and interest rates.

- Cash reserves provide lenders with confidence.

- Employment stability shows predictability.

A borrower with moderate income and low debt may be approved more easily than a high earner with large student loans and luxury car payments.

If You’ve Already Been Denied

A denial is not permanent.

You can:

Spend three to six months paying down debt

Explore different loan products

Work with a mortgage broker who has access to multiple lenders

Adjust your price range

Small changes in DTI can completely change the outcome.

Know Your Number Before You Apply

Many buyers focus on credit scores and down payments while ignoring DTI. Yet this ratio often determines approval.

Calculate your DTI before speaking with a lender. If it is high, allow 60 to 90 days for improvement. Paying down balances, avoiding new debt, and strengthening your income position can dramatically improve your chances.

The goal is not just to get approved. It is to secure a mortgage payment that fits your life comfortably.

Understanding your DTI gives you clarity. And clarity gives you control.

Contact us to learn more about our Realtor® representation when buying or selling your West Village Of Shirlington home? Receive a free property evaluation by heading to our market analysis page, where we will provide a Comparative Market Analysis (CMA) on your property for you!

Posts by Categories

- Arlington VA Real Estate (12)

- Homeowner Guides (6)

- Northern Virginial real estate (6)

- Choosing a Realtor (5)

- Rosslyn Real Estate (4)

- McLean Real Estate (4)

- Aldie Real Estate VA (4)

- Buying a Home (3)

- Fairfax County VA Real Estate (3)

- Neighborhoods in Arlington, VA (3)

Posts by Month

- August, 2026 (3)

- July, 2026 (5)

- June, 2026 (9)

- May, 2026 (15)

- April, 2026 (11)

- March, 2026 (12)

- February, 2026 (8)

Related Blogs

What are the drawbacks or limitations of Virginia’s first-time home buyers' programs?

Buying your first home in Virginia is exciting. It’s also expensive. Between the down payment, closing costs, and rising home prices in areas like Northern Virginia, Richmond, and Hampton Roads, many first-time buyers feel priced out before they even start. That’s where Virginia’s first-time home buyer programs come in.Most of these programs are administered through Virginia Housing, the state’s

First Time Home Buyer Guide Northern Virginia

Are you a first-time home buyer in Arlington, Virginia? Here’s what you need to know about first-time home buyer programs in Virginia — and how to compete in Arlington’s dynamic housing market.Buying your first home is one of the biggest financial decisions you’ll make. That’s why we created this comprehensive guide covering financing options, grants, Virginia assistance programs, and the full h